The year 2024 was marked out for the fact that there were almost four dozen elections taking place in many countries throughout the world. It is also the year in which the highest number of countries in sub-Saharan Africa recorded concerning degree of debt distress with the possibility of defaults becoming undeniable.

The burden of both domestic and foreign debt is real for these countries and despite the announcements that all is positive, we think that for the majority of these countries, the light at the end of the tunnel is yet to be seen.

The short history of this is that because of the heavily indebted poor countries (HIPC) Initiative, 31 countries in sub-Saharan Africa had received substantial debt write offs and therefore had a good platform to build upon into growth and prosperity. While Kenya, for example, chose not to benefit from the HIPC Initiative, some economic and political changes in the country renewed belief that it too stood on a great platform to raise growth levels and reduce poverty among its citizens.

The report card in 2024 shows that countries that benefited from HIPC relief have come full circle and are back in debt distress. For most of the period after the turn of the millennium, Kenya and its neighbours on the continent seemed to be getting things right, hence the nickname “Africa Rising”. Kenya’s case illustrates exactly what its leadership, some of its people and its world cheerleaders got wrong. Its example can be generalised to the rest of the countries in distress, except that Kenya’s Treasury is not dependent on high mineral resource rents because the country has no significant mineral reserves.

Kenya’s story

At the end of 2021, Kenya went into an IMF programme and this predictably set Kenya’s macroeconomic policy. In a study, ‘And Then Floods..’, two staff of the Institute of Economic Affairs and an independent researcher track Kenya’s performance over 30 years. They conclude that Kenya’s debt distress at the end of 2021 was a symptom of consistent macroeconomics errors that are separate from the corruption and its position as a small and open economy.

In the 30 years from 1990 to 2020, Kenya’s growth rate measured in 2017 US dollars was equivalent to 0.81% per annum. Starting with a sub US$2,000 income per citizen, this growth rate would require 88 years to double. This poses a problem for external debt management in foreign currency, as it suggests that accumulating debt at an interest rate above 1% will inevitably lead to payment difficulties. And that is certainly what Kenya continues to face.

It is worth noting that the policy context for this whole generation of time was not similar because in Kenya’s case it straddled two epochs, with the first half showing comparatively tight fiscal policy conditioned by the imperative for repayment of debt. From 2013, Kenya saw an unprecedented fiscal expansion proceeding the cheerleading of the Africa Rising narrative. The growth that coincided with this fiscal expansion was low quality, as it not only depressed business investment but also generated lower poverty reduction per percentage point of growth. Summarising both epochs leaves no doubt to dispassionate minds that misspecified fiscal policy has been costly for Kenya and, by extension, other countries in sub-Saharan Africa.

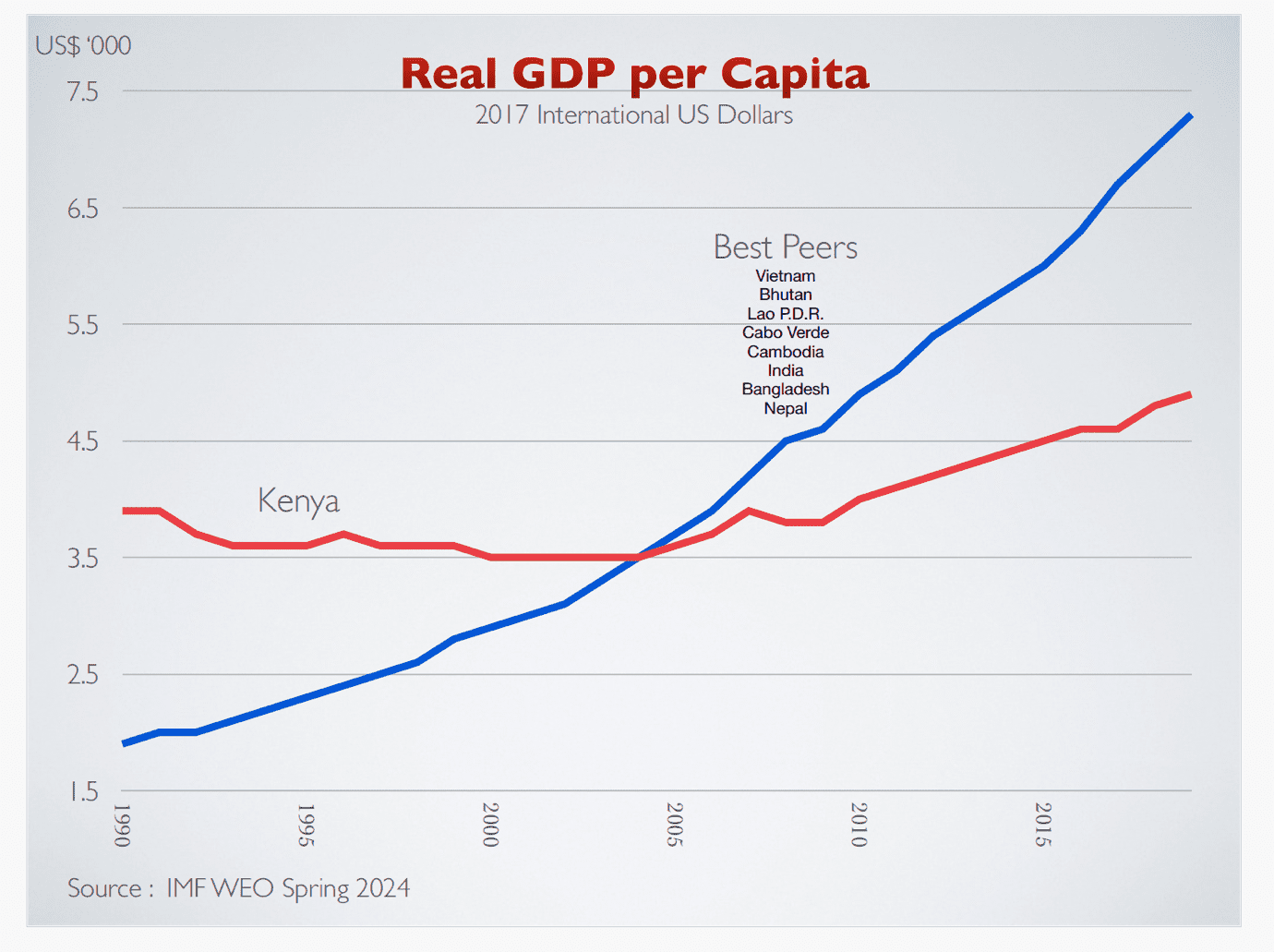

And yet the combined effect of the misspecified fiscal policy and Kenya’s low growth rate leads to an unsettling realisation but one that is relevant to the position on debt distress. Throughout the generation traced by these authors, we found that Kenya underperformed its global peers against which to measure its 1990 development trajectory. As the chart 1 shows, Kenya has underperformed the best performers who in 1990 had comparable economic and social indicators. And this underperformance is not marginal. These peers qualify as Kenya’s appropriate comparators because they started from similar development characteristics with nearly half of them having worse indicators than Kenya had in 1990.

Chart 1: Kenya’s GDP per capita growth against global peers in US$ 2017 equivalent (1990-2019)

As the Chart 1 illustrates, the average growth rate for many of these countries was several times higher than Kenya’s and they maintained this growth rate for an entire generation, with all of them escaping the status of high poverty among citizens. ‘Had Kenya’s GDP per capita grown at the same rate as the average for these peers, Kenya’s GDP per capita at the even of Covid-19 would have been more than thrice its reality’.

We refer to this as foregone growth or the growth benefit that Kenya left on the table owing to wrong macroeconomics policy. This is not a trivial issue because leaving all factors constant would place Kenya within 20% of the income level of China in 2019 and Kenya would also qualify as a growth miracle of the last generation. This growth level would have reduced poverty rates to less than a third of their reported figure of 33% in 2019.

Like many countries in sub-Saharan Africa, Kenya flattered itself between 2000 and 2010 with intermittent high growth rates for a year or two, but failed to maintain a consistent growth trajectory. Against that background, sound macroeconomics policy was not in place and the borrowing spree from both domestic and external sources failed to yield the desired growth rates to make debt payable upon maturity.

The last generation is one that started on a sad note of high indebtedness, got better with painful adjustments to cope with repayment and then the hubris followed with little growth recovery. All this culminated in a resounding thud precipitated but not caused by Covid-19, into debt distress and real risk of defaults and necessary restructuring.

In short, like Kenya, most of the countries facing acute debt distress and the few that have defaulted failed to keep up with growth as their global best peers did due to deficiencies in macroeconomics management. The lost potential in economies that lacked vitality is high, and the citizens will again pay a high price for it. Macroeconomic mistakes perpetuated over a generation are expensive and even shorten lives, as Kenya’s Generation Z protests on the streets of Nairobi in June 2024 proved.