Africa’s development story over the past decade has been marked by an uneasy reliance on external borrowing. World Bank’s International Debt Report 2023 noted that developing countries spent a record $443.5 billion to service their external public and publicly guaranteed debt in 2022. Sub-Saharan African countries between 2013 and 2022 witnessed a surge in external debt composed largely of long-term debt and public Sector debt. This external debt-weighty model has exposed the region to burdensome repayment pressures coupled with rising interest costs and volatility around FOREX that inadvertently threatens long-term fiscal sustainability.

Africa’s reliance on external borrowing, coupled with weak governance in contracting, managing, and repaying debt, has eroded fiscal strength and heightened vulnerability to shocks. Opaque fiscal practices, inconsistent repayments, and limited accountability further deepen the crisis. The continent’s debt burden, rooted in governance gaps prevents the rebalancing of liabilities, discourages stable long-term capital and FDI, perpetuates exposure to risks, and obstructs the path toward sustainable growth and freedom from external dependence.

Moving beyond borrowing requires that Africa recognize that debt-resilience as inseparable from political and fiscal governance. Transforming and rotating Africa’s debt paradox into a premeditated development tool must underpin the continent’s economic sovereignty and resilience. Africa’s debt challenge is inseparable from governance. We must examine fiscal governance and debt sustainability in Africa while identifying pathways toward a debt-resilient future for Africa.

Africa and Shared Debt Dynamics (2013–2023)

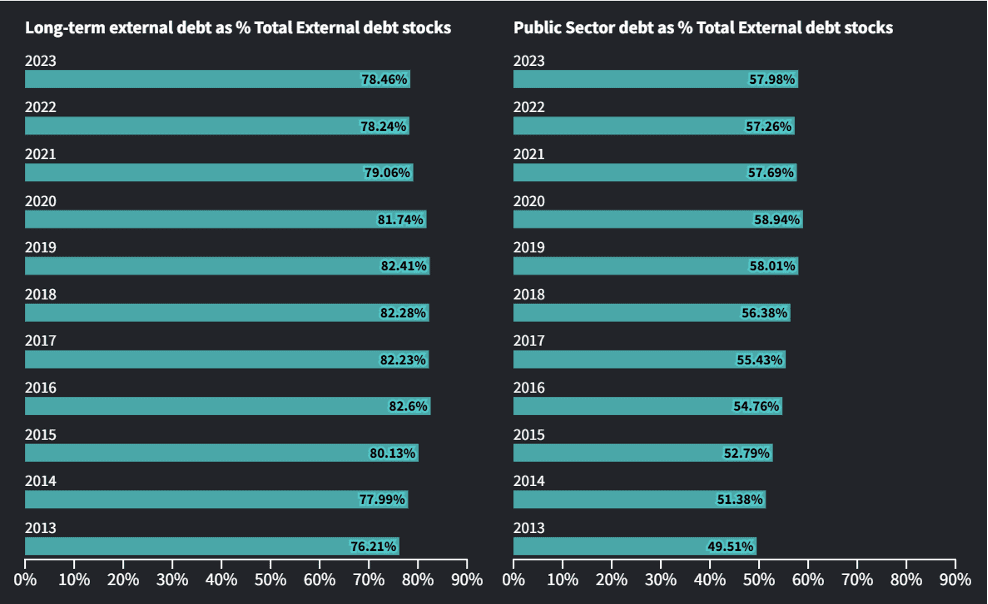

Categorising sub-Saharan Africa’s debt dynamics as percentages of total external debt stocks indicates that the region’s debt structure is dominated by long-term debt, which consistently accounts for over three-quarters of total external debt stocks. This pointer, which stood at 76.2% in 2023, rose to 80.13% in 2015, averaged 82% between 2016 and 2019 before revolving around 78–79% by 2022–2023.

Similarly, public sector debt as a percentage of total external debt stock rose steadily from 49.5% in 2013 to nearly 59% in 2019–2020, and slackening to 57–58% by 2022–2023. It evidently portrayed Governments as the primary borrowers, underscoring weak private sector participation in external financing.

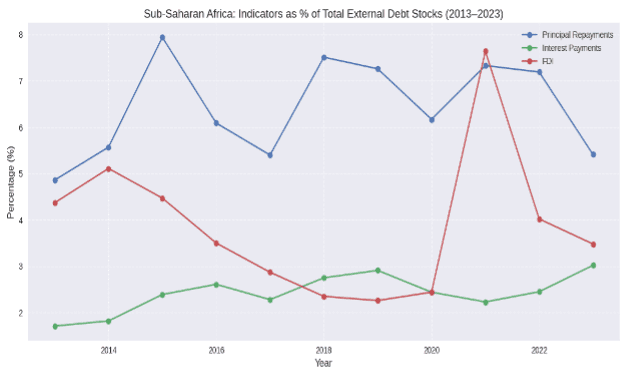

Capturing the trajectory of debt servicing pressures, principal repayments as a share of total external debt stocks fluctuated between 5–8%, peaking at 7.9% in 2015 and 7.3% in 2021 before easing to 5.4% in 2023. This volatility reflects refinancing cycles and repayment pressures around weak revenue bases. In contrast, interest payments rose steadily from 1.7% in 2013 to 3.2% in 2023, underscoring rising borrowing costs and growing reliance on non-concessional financing. Although servicing ratios remain relatively low, the upward trend in interest payments signals mounting fiscal strain, with debt service increasingly crowding out resources for development priorities.

Encapsulating the scale and volatility of Foreign Direct Investment (FDI) relative to debt stocks highlights how small FDI is in relation to Africa’s debt burden. FDI inflows as a share of debt stocks declined steadily from 5.1% in 2014 to 2.3% in 2018–2019, underscoring their limited role in offsetting rising debt. A temporary rebound in 2021 lifted the ratio to 7.6%, but by 2023 it fell to 3.5% highlighting the volatility over investment inflows. Generally, FDI remains small compared to debt, and its instability reflects fragile investor confidence, fiscal vulnerabilities, and policy unpredictability. This emphasizes that without stronger public governance and a more predictable investment climate, FDI cannot contribute significantly in counterbalancing Africa’s debt dependence.

Growth in total external debt stocks, long-term obligations, public sector borrowing, principal repayments, interest payments, and foreign direct investment raise serious concerns about Africa’s reliance on sovereign debt. The trends further highlight weaknesses in fiscal governance, transparency, and debt sustainability, particularly against the backdrop of volatile revenues.

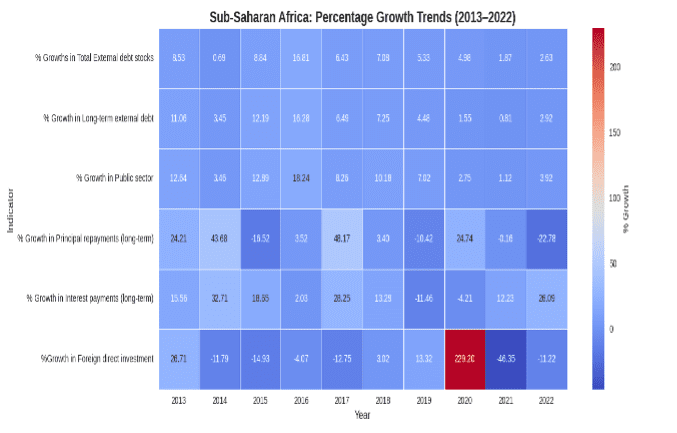

Sub-Saharan Africa’s debt trajectory between 2013–2022 tells a story of rapid accumulation in the mid-2010s, peaking in 2016, followed by a sharp slowdown as fiscal pressures mounted and borrowing capacity weakened. Public sector borrowing drove this surge, with growth rates exceeding 18% in 2016. Afterwards, public sector debt growth slowed sharply, averaging just 3% by 2022, as tighter global conditions, rising servicing costs, and concerns over sustainability constrained borrowing capacity. Debt servicing pressures added to volatility. Principal repayments spiked in 2014 and 2017 but contracted in 2022 amidst debt-restructuring, while interest costs surged in 2014 and 2017 and fell during COVID-19’s monetary easing while exposing weak debt management frameworks. Borrowing remains essential for development, but the trajectory reveals a fragile balance as Africa risks being trapped in cycles of debt dependence and financial vulnerability.

Between 2013 and 2023, SSA FDI in million USD ranged from 20,623.40 in 2013 to 16,413.70 in 2018 to a peak of 63,079.60 in 2021, declining to 30,044.10 in 2023, a highly volatile trajectory. The 2020–2021 229.20% surge stemmed mainly from statistical variances, and mega‑projects in Mozambique’s LNG and Congo’s mining sectors, not broad improvements in SSA’s investment climate. Post‑2021, inflows stabilized above mid‑2010s levels but remain far below the peak highlighting that FDI cannot reliably contribute in offsetting Africa’s debt dependence.

Debt Sustainability, GNI for Sub-Saharan Africa (2013–2023)

The IDR 2024 debt sustainability indicators for SSA within the decade was characterised by rising debt burdens, high servicing costs, declining reserves, and increasing reliance on multilateral lenders.

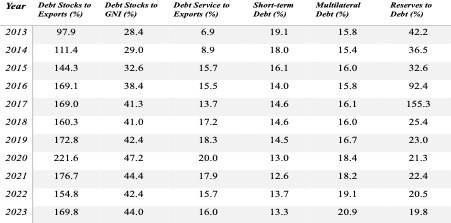

External debt relative to exports surged from 97.9% (2013) to 221.6% (2020), showing that debt grew faster than export earnings, though easing at 169.8% (2023), it remained high. External debt to GNI also climbed steadily, signalling heavier obligations relative to national income. Debt service-to-exports rose from 6.9% (2013) to 20% (2020), and stabilizing around 16% (2023), indicating persistent repayment strain and high debt service costs. Short-term debt to external debt stock declined from 19.1% (2013) to 13.3% (2023), reducing rollover risk. Meanwhile, multilateral to external debt rose from 15.8% to 20.9%, showing greater reliance on institutions like the IMF and World Bank. Reserves-to-external-debt peaked at 155% (2017) but fell sharply to 19.8% (2023), suggesting reserves collapse and leaving countries with far less buffer against repayment shocks.

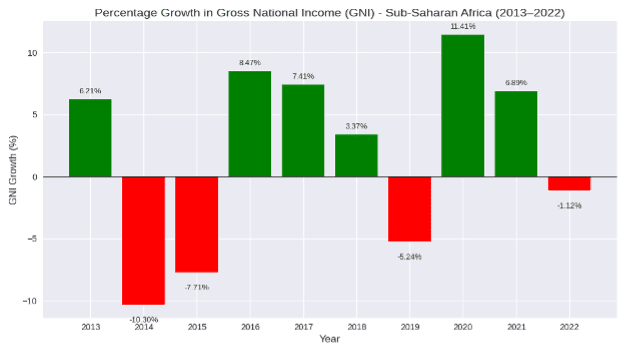

Between 2013–2022, SSA’s GNI growth saw sharp contractions (2014, 2015, 2019, 2022), rebounds (2016–2017), and uneven recovery. Growth slowed again in 2018–2019, exposing vulnerability to shocks and fiscal strain. Despite COVID-19 disruptions, GNI surged in 2020–2021 with stimulus-driven recovery, but dipped in 2022, reflecting persistent debt burdens, weak investment, and fragile governance.

Sharp GNI swings reflect external shocks, commodities instability, and debt pressures, exposing structural regional vulnerability. While rebounds are possible, sustained stability requires stronger fiscal governance, diversified export and earnings, and resilient financing strategies to smooth growth

Findings, Conclusion and Policy Recommendations

Findings show Africa’s debt burden rising faster than exports and GNI, with servicing costs eroding fiscal space and reserves, increasing vulnerability to shocks and reliance on multilateral debt. Public financing remains debt-heavy and state-driven, with borrowings surging in 2016 but slowing after 2021 amid distress and creditor caution. Furthermore, repayments and interest costs have been volatile, exposing weak revenue bases and reliance on costly non-concessional loans. Repayments swung from 43.7% growth in 2014 to -22.8% in 2023, reflecting refinancing pressures and weak revenues, while interest costs spiked in 2014 and 2017, dipped in 2019, and rose again in 2022. FDI inflows remain small and unstable, highlighting fragile investor confidence and policy unpredictability. GNI growth remained uneven, contractions in 2014, 2015, and 2019, a rebound in 2020–2021, and a renewed reduction in 2022.

Africa’s debt crisis is not simply about rising liabilities, it is united with a governance challenge, and the trajectory is unsustainable. Weak fiscal institutions, opaque debt contracts and spendings, and limited domestic resource mobilization have left countries trapped in cycles of borrowing and refinancing alongside its vulnerabilities. Without stronger basic governance reforms, fiscal discipline, transparency, and predictable policies to attract stable FDI, diversify exports, and grow GNI sustainably, Africa risks remaining entombed in sovereign debt dependence and limited private investment. By fusing governance with resilience, African economies can shift from reactive debt dependence to proactive fiscal sovereignty, creating space for stable investment inflows and sustainable growth.

A deliberate shift toward concessional financing, debt reprofiling, and swaps (debt-for-climate, debt-for-health, etc) where debt relief is tied to investments in productive sectors should be imminently pursued. Strengthening of political will, fiscal and governance transparency, and rule of law to rebuild investor confidence and reduce hidden liabilities should be vigorously practised. Forecasting capacity and rebuilding of reserves to manage repayment cycles should be improved.

Strengthening domestic resource mobilization through broader tax bases, reduced illicit financial flows, and digital systems requires rebuilding public trust. Stable tax regimes, investment laws, and trade policies are vital to attract FDI, while diversification beyond extractives, Leveraging AfCFTA and infrastructure investment can reduce commodity dependence. Debt must align with national priorities and self-liquidating infrastructures to avoid cycles of refinancing. Regional bargaining through the AU alongside a Pan-African Credit Rating Agency is essential for fairer debt pricing.

Transparent debt management, credible institutions, and disciplined fiscal policies form the foundation of resilience against unsustainable debt. By uniting governance, leadership, and resilience, Africa can move from reactive debt dependence to proactive economic sovereignty.